UK inflation rises, adding to pressure on rates

There are two key domestic issues this week for UK financial markets. One is the latest inflation news and the implications for interest rates. The second is the ongoing Brexit discussions and what might the latest phase imply for settling. Let's focus here on the inflation news.

This week's data release showed that inflation rose by 3 percent in the year to September, a five and a half year high. The likelihood is that inflation will rise further in coming months, a point that the Governor of the Bank of England made in testimony he gave to the Treasury Select Committee. This, however, has already been discounted by the markets for some time.

UK Consumer Price Index

Source: ONS

Inflation peak point

Regular readers may recall that earlier this year we said that we expected inflation to peak around 3.5 percent in the fourth quarter. At that time this forecast was significantly higher than the below 3 percent peak then being projected by the Bank, and above market consensus, but it was by no means the most pessimistic forecast at that time. In mid summer we did see two successive months when the inflation releases were "good", raising the possibility of inflation peaking lower and sooner. But that proved illusory and inflation continued to rise. In May, annual inflation was 2.9 percent, before falling to 2.6 percent in June and July, rising again in August to 2.9 percent before this latest increase in September.

We stick with our view of a peak this fourth quarter. Whether it reaches 3.5 percent remains to be seen. Still, we then expect inflation to head lower as we move through 2018. That, in itself, should be good news for consumer spending and the economy. The full extent of any boost will also depend on what happens to wages. Real incomes – and hence spending power – have been squeezed by the spike in inflation, and an unwinding of this effect will ease the pressure on consumers.

Pessimistic growth forecasts?

Data released this week showed that in the 3 months to August, wages (including bonuses) rose at an annualized rate of 2.2 percent and 2.1 percent excluding bonuses, but in real terms (which means taking into account inflation) the figures were, respectively, a fall of 0.3 percent and of 0.4 percent. These wage figures were released alongside employment data that suggests a robust economy. Employment reached 32.1 million in August. In the last three months (June to August) employment is up 94,000 from the previous three months and 317,000 from a year earlier. The employment rate reached another all-time high of 75.1 percent and the unemployment rate fell to 1.44 million, still high but at least heading in the right direction. Over the last three months unemployment is 52,000 down from the previous three months and 215,000 lower than a year ago.

Although the UK economy had slowed slightly this year, as the market expected, these healthy jobs figures show there is still some strength. Also, the balance of growth has improved, with a rise in investment and exports. Perhaps growth forecasts for 2018 may yet prove too pessimistic, exemplified by the Organisation for Economic Cooperation and Development (OECD) this week predicting only 1 percent growth in 2018. Closer to 2 percent is more likely.

Much will depend on monetary policy and how the Bank of England responds to the latest inflation news. The Bank has a 2 percent inflation target. Throughout much of this year the Bank has indicated that they would look beyond the current rise in inflation which is largely a feed through from the weaker pound. Their focus, they have made clear, would be what is happening to domestic inflation. This has remained relatively subdued. In addition the Bank has, sensibly, been reluctant to tighten in the face of a possible slowdown in the economy. Last month the vote was 7-2 to leave rates on hold.

Implication for interest rates

The way I have interpreted the Bank is that rates will stay low, rise gradually and peak at a low level. That is still the broad message. Now, however, the emergency rate cut that took place in the aftermath of the referendum looks set to be removed. At that time we agreed with the rate cut and further quantitative easing, but not with the corporate bond buying. The latter, in our view, has still not been justified fully.

Offsetting influences

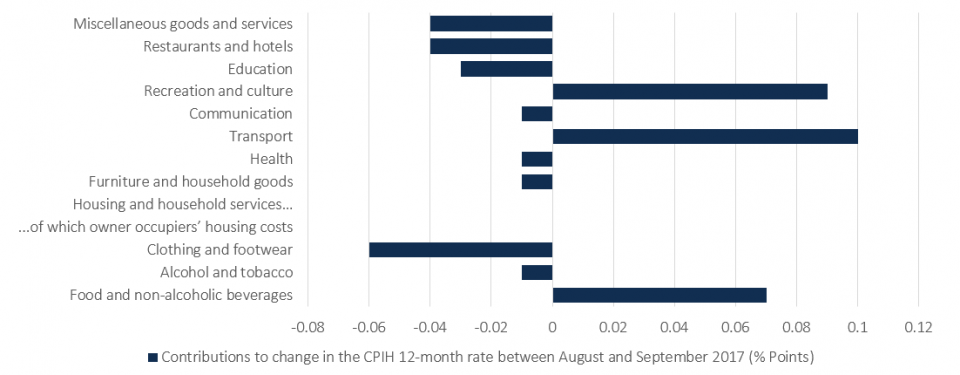

The breakdown of the inflation data does, however, highlight many offsetting influences, and to calculate the annual increase one needs to make a comparison with what happened a year ago. 8 of the 12 main categories that make up the consumer price index saw their annual rate of inflation ease in September, but these were not enough to offset the upward effect from other components. The biggest annual increase was in transport costs, where prices fell less than they did a year ago. Food and recreational goods prices rose on the year, the latter reflecting computer game prices. While clothing prices rose, they increased by less than they did a year ago. Perhaps this – plus uncertainty about the economic outlook – highlights why the Bank's decision is not certain.

Contributions to change in 12m CPIH rate between August and September 2017

Source: ONS

Note: 1. CPIH extends the more well known CPI measure to include costs associated with owning, maintaining and living in one’s own home, 2. Individual contributions may not sum to the total due to rounding.

Next rate rise

In our view, we think rates should, and will rise, this November. I have always thought the Bank could tighten in smaller steps – one-eighth of one per cent, 0.125 percent – to highlight that they are being gradual, and in order to minimise the danger of people, firms and the financial markets over reacting. But they have not indicated that they are thinking this way. Instead a 0.25 percent hike is likely to be the first step. In the wake of the recent IMF meetings in Washington the message the Bank may have returned with is global growth is increasing. Moreover the mindset of central bankers in Washington also seemed to be that there remain medium-term downside economic risks and thus it may be important to build up a buffer now, lest it needs to be used in a few years time to counteract a slowdown. That buffer is, indeed, higher rates. Thus the first step in UK interest rate normalisation may not be too far away.

How markets will react to rates heading higher is always difficult to predict. Because a rate hike has been talked about for some time, and now is discounted, there will be a natural tendency for markets to think they will handle this smoothly. But it also needs to be seen alongside other factors, including domestic economic data and how the Bank of England goes about reversing its printing of money as it reduces the size of its balance sheet. This could have a direct impact on gilt yields. Also, the external environment cannot be overlooked as the possibility of policy tightening by central banks elsewhere could impact global markets. Then, there is the Brexit negotiations and how they might impact sterling. Overall, we are now closer to the peak in UK inflation but also closer to the start of policy normalisation, which when it comes should be gradual and well signalled.