Which of the major stockmarkets are ‘cheap’ going into 2018?

Finding value in stock markets at present is like looking for the sixpence in a Christmas pudding. It’s there but it’s hard work finding it. Others round the table are likely to end up disappointed.

Stock markets have been on quite a run for several years now and 2017 has failed to disappoint. Unfortunately for investors, the gifts of those Christmases-past means that there is little left on the table for this year.

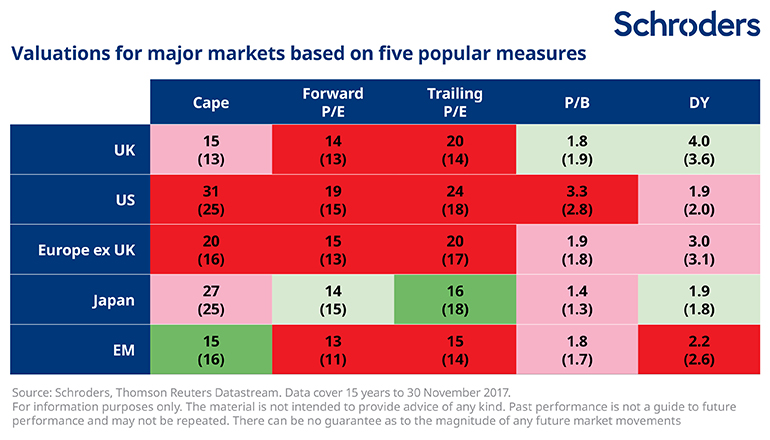

The table below shows a number of valuation indicators compared with their average (median) of the past 15 years, across five different regional equity markets. A description of each valuation indicator is provided at the end.

Figures are shown on a rounded basis and have been shaded dark red if they are more than 10 per cent expensive compared with their 15-year average and dark green if more than 10 per cent cheap, with paler shades for those in between.

As if a glass of red wine has been spilled over it, the table is stained red. With perhaps the exception of Japan, expensiveness abounds. No market is unequivocally cheap so all come with a health warning.

Japan stands out as the one market which could arguably make a case for being attractively valued.

It offers an above-average dividend yield and is cheap on a price/earnings basis. It also has the added support that profit margins are expanding and both monetary and fiscal policy are supportive.

However, even here some valuation indicators are on the expensive side and the market is highly exposed to risks from protectionism and North Korea.

Emerging markets have had a very strong 2017, returning more than 30 per cent and outperforming developed markets in the process.

However, prices have now shifted to expensive territory on most bases and returns may moderate significantly.

Within the other major developed markets, there are slim pickings. The UK hints at cheapness but is very expensive on a trailing price/earnings basis and is heavily reliant on the oil price recovery holding out, due to oil companies making up such a large chunk of the market.

Brexit, of course, cannot be forgotten, although any weakness in sterling should benefit overseas earners and may provide a counterbalance to domestic weakness.

Europe is better placed than valuations would suggest. A cyclical recovery is underway and there is room for profit margins to expand and support earnings and stock market returns.

The US sticks out as being the most expensive market, but this is nothing new. It has been the case for a number of years.

Furthermore, the Trump administration’s tax reduction plans should provide a short term boost to corporate profitability and underpin prospects. Valuations are highly likely to count against the US market in the long term, but they are rarely in themselves the reason why markets take a turn for the worse.

Of course, past performance offers no guide to the future and your capital is at risk with any investment.

- Investors expect returns of 10.2 per cent over the next five years – millennials want more

- 14 years of returns – history's lesson for investors

- The FTSE 100 in 2017: Five charts that tell the story

Five ways to measure stock market value – with pros and cons for each

Valuation is key to making investment decisions. Invest when markets are expensive and future returns are more likely to be poor over the medium to long term. Buy when markets are cheap and the odds are stacked much more in your favour.

But a word of warning – valuations are useless at predicting stock market behaviour over short timeframes when fear, greed and other noisy factors tend to dominate.

When considering equity valuations there are many different measures that investors can turn to. Each tells a different story. They all have their benefits and shortcomings so a rounded approach which takes into account their often-conflicting messages is the most likely to bear fruit.

Forward P/E

A common valuation measure is the forward price-to-earnings multiple or forward P/E. We divide a stock market’s value or price by the aggregate earnings per share of all the companies over the next 12 months. A low number represents better value.

An obvious drawback is that no one knows what companies will earn in future. Analysts try to estimate this but frequently get it wrong, largely overestimating and making shares seem cheaper than they really are.

Trailing P/E

This is perhaps an even more common measure. It works similarly to forward P/E but takes the past 12 months’ earnings instead. In contrast to the forward P/E this involves no forecasting. However, the past 12 months may also give a misleading picture.

This is particularly true if earnings have slumped but are expected to rebound. For example, UK equities are very expensive on this measure at present, partly because of past commodity price declines and the UK market’s large commodity exposure.

CAPE

The cyclically-adjusted price to earnings multiple is another key indicator followed by market watchers, and increasingly so in recent years. It is commonly known as CAPE for short or the Shiller P/E, in deference to the academic who first popularised it, Professor Robert Shiller.

This attempts to overcome the sensitivity that the trailing P/E has to the last 12 month’s earnings by instead comparing the price with average earnings over the past 10 years, with those profits adjusted for inflation. This smooths out short-term fluctuations in earnings.

When the Shiller P/E is high, subsequent long term returns are typically poor. One drawback is that it is a dreadful predictor of turning points in markets. The US has been expensively valued on this basis for many years but that has not been any hindrance to it becoming ever more expensive.

Price-to-book

The price-to-book multiple compares the price with the book value or net asset value of the stockmarket. A high value means a company is expensive relative to the value of assets expressed in its accounts. This could be because higher growth is expected in future.

A low value suggests that the market is valuing it at little more (or possibly even less, if the number is below one) than its accounting value. This link with the underlying asset value of the business is one reason why this approach has been popular with investors most focused on valuation, known as value investors.

However, for technology companies or companies in the services sector, which have little in the way of physical assets, it is largely meaningless. Also, differences in accounting standards can lead to significant variations around the world.

Dividend yield

The dividend yield, the income paid to investors as a percentage of the price, has been a useful tool to predict future returns.

A low yield has been associated with poorer future returns.

However, while this measure still has some use, it has come unstuck over recent decades.

One reason is that “share buybacks” have become an increasingly popular means for companies to return cash to shareholders, as opposed to paying dividends (buying back shares helps push up the share price).

This trend has been most obvious in the US but has also been seen elsewhere. In addition, it fails to account for the large number of high-growth companies that either pay no dividend or a low dividend, instead preferring to re-invest surplus cash in the business to finance future growth.

A few general rules…

Investors should beware the temptation to simply compare a valuation metric for one region with that of another. Differences in accounting standards and the makeup of different stockmarkets mean that some always trade on more expensive valuations than others.

For example, technology stocks are more expensive than some other sectors because of their relatively high growth prospects.

A market with sizeable exposure to the technology sector, such as the US, will therefore trade on a more expensive valuation than somewhere like Europe. When assessing value across markets, we need to set a level playing field to overcome this issue.

One way to do this is to assess if each market is more expensive or cheaper than it has been historically, as we have done above.

Finally, investors should always be mindful that past performance and historic market patterns are not a reliable guide to the future.

Important Information: The views and opinions contained herein are those of Duncan Lamont, Head of Research & Analytics, and may not necessarily represent views expressed or reflected in other Schroders communications, strategies or funds. This material is intended to be for information purposes only and is not intended as promotional material in any respect. The material is not intended as an offer or solicitation for the purchase or sale of any financial instrument. The material is not intended to provide and should not be relied on for accounting, legal or tax advice, or investment recommendations. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Past performance is not a guide to future performance and may not be repeated. Exchange rate changes may cause the value of any overseas investments to rise or fall. The value of investments and the income from them may go down as well as up and investors may not get back the amounts originally invested. All investments involve risks including the risk of possible loss of principal. Information herein is believed to be reliable but Schroders does not warrant its completeness or accuracy. Reliance should not be placed on the views and information in this document when taking individual investment and/or strategic decisions. Some information quoted was obtained from external sources we consider to be reliable. No responsibility can be accepted for errors of fact obtained from third parties, and this data may change with market conditions. This does not exclude any duty or liability that Schroders has to its customers under any regulatory system. The opinions in this document include some forecasted views. We believe we are basing our expectations and beliefs on reasonable assumptions within the bounds of what we currently know. However, there is no guarantee than any forecasts or opinions will be realised. These views and opinions may change. Issued by Schroder Investment Management Limited, 31 Gresham Street, London EC2V 7QA. Registration No. 1893220 England. Authorised and regulated by the Financial Conduct Authority.